Hiring Accountants and Tax Professionals: Benefits, Costs, Outsourced Services, and Expert Tips

Managing money is one of those things most business owners and busy individuals would rather avoid until the last possible minute. Receipts pile up, deadlines creep closer, and suddenly you’re staring at a shoebox full of expenses, wondering if you’re going to owe the IRS a small fortune. I’ve been there, and so have thousands of clients I’ve worked with over the years. The good news? Hiring the right accounting and tax help in 2025 doesn’t have to be complicated or painfully expensive. In fact, it can save you far more than it costs.

Whether you’re a solopreneur in Denver, a growing startup, or someone who just wants to stop stressing every April, this guide will walk you through everything you need to know this year: the real benefits, what things actually cost, when outsourcing makes sense, the difference between bookkeepers and accountants, and a handful of tips that can keep thousands of dollars in your pocket.

Why Professional Accounting and Tax Help Still Matters

Tax laws didn’t get simpler while we were all busy updating software and chasing inflation. If anything, remote work, side gigs, crypto, and new deductions for energy-efficient business purchases have made things messier. A good tax expert does more than fill out forms. They spot deductions you’d never find on your own, help you avoid audits, and free up dozens (sometimes hundreds) of hours you can spend actually growing your income instead of chasing receipts.

Even basic bookkeeping errors can cost serious money. One missed quarterly estimate, one misclassified expense, or one overlooked credit, and you’re looking at penalties that add up fast. Working with someone who lives and breathes this stuff day in and day out is still the smartest insurance policy most people never buy, until they need it.

The Real Benefits of Outsourcing Your Accounting

More businesses than ever are ditching the in-house spreadsheet hero and moving to outsourced accounting and bookkeeping services. Why? Because payroll, sales tax in multiple states, inventory accounting, and monthly reconciliations eat time like nothing else.

When you outsource, you get an entire team for less than the fully-loaded cost of one full-time employee. No benefits, no vacation pay, no training when the rules change again. Many firms now use cloud software that gives you real-time dashboards, so you’re never in the dark about cash flow. And if something goes wrong, the liability usually sits with the provider, not you.

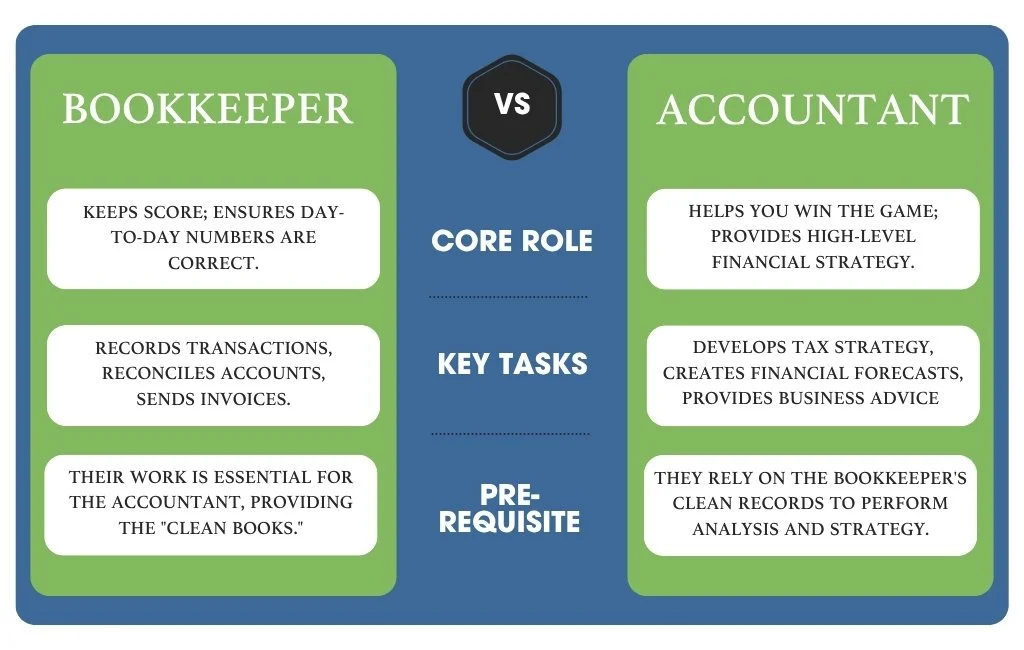

Bookkeeper vs. Accountant: Which One Do You Actually Need?

This is the question I get asked more than any other. The short version: bookkeepers keep score, accountants help you win the game.

A bookkeeper records transactions, reconciles accounts, sends invoices, and makes sure the day-to-day numbers are correct. An accountant takes those clean books and turns them into tax strategy, financial forecasts, and advice on whether you should buy that new equipment this year or next.

Most small businesses need both, but not both full-time. Many of our clients use Denver bookkeepers for the weekly grind and only bring in a CPA during planning season or when something big is happening (raising funding, selling the business, etc.). It’s the combo that saves the most money.

There’s also a surprising overlap between bookkeeping and tax preparation. Good bookkeepers already categorize everything in a tax-friendly way, which means your accountant spends less time (and you spend less money) when filings roll around.

When to Hire an Accountant (And When You’re Just Wasting Money)

Not every 1099 freelancer needs a full-time CPA. Here are the moments most people wish they’d brought in help sooner:

Your revenue crosses $250,000

You have employees or contractors in multiple states

You’re buying or selling real estate

You received a letter from the IRS (any letter)

You’re considering an S-Corp election or other entity change

Retirement planning actually matters to you now

If none of those apply and your situation is truly simple, decent software plus a one-time review might be enough. But the minute life or business gets complicated, the cost of doing it yourself usually exceeds the cost of hiring a tax accountant in Denver who already knows the local rules inside out.

How Much Does an Accountant Actually Cost in 2025?

Costs vary wildly depending on where you are and what you need. Here’s what we’re seeing right now:

Monthly bookkeeping: $300–$1,500 (depends on transaction volume)

Individual tax return (Schedule C or basic investment income): $500–$1,500

Small business tax return (LLC or S-Corp): $1,200–$4,000

Payroll processing: $50–$150 per month + $5–$12 per employee

Year-round tax planning + quarterly reviews: $250–$800 per month

Yes, that sounds like real money. But compare it to the alternative: one missed deduction on a $500,000 revenue business can easily cost $10,000–$20,000 in extra taxes. Most clients recoup the entire annual fee in the first year through better planning alone.

Why Local Still Matters (Even When Everything’s Cloud-Based)

You can hire someone in another state, sure. Plenty of people do. But when you need to sit across from someone and explain why that $8,000 home office renovation should be a deductible improvement and not a repair, local help. Denver has its own sales-tax quirks, Colorado-specific credits, and a surprisingly active audit division. Firms that live here know the auditors by name, which matters more than most people want to admit.

That’s why so many owners still look for a tax accountant in Denver even when half their team works remotely.

Expert Tips That Save the Most Money in 2025

Start tax planning services in July, not January. The best deductions are created, not found.

Pay yourself a reasonable salary if you’re an S-Corp. Too low and the IRS will recharacterize dividends as wages (and hit you with back taxes).

Track every mile and every home-office expense properly from day one. The IRS is cracking down hard on sloppy records.

Bundle one-time cleanup projects instead of paying monthly for messy books. A $3,000 catch-up is usually cheaper than twelve months of high fees on chaotic data.

Ask about flat-fee pricing for personal tax services or business tax services so you’re never surprised by the final bill.

The Hybrid Approach Most Successful Clients Use

Here’s what actually works for the majority of businesses under $5 million in revenue:

An outsourced bookkeeping team is handling the daily work through cloud software

Quarterly review calls with a CPA who knows your big picture

Year-round access to tax planning services so nothing slips through the cracks

One predictable monthly payment instead of surprise bills every spring

It’s the sweet spot between doing everything yourself (and risking expensive mistakes) and hiring a full-time CFO you don’t need yet.

Final Thought

The real cost of accounting and tax help isn’t the invoice. It’s the peace of mind that comes from knowing someone smarter than you about this stuff has your back. In 2025, the rules are still changing, audits are up, and the difference between average advice and great advice can literally be six figures over a few years.

Whether you decide to keep things in-house, go fully outsourced, or land somewhere in between, just make the decision intentionally instead of letting April force your hand again.

If you’re in Colorado and want to talk through what makes sense for your specific situation, the easiest next step is reaching out to one of the best accounting companies in Denver, CO, and scheduling a no-pressure conversation.

Frequently Asked Questions

-

Absolutely. Software handles data entry, but it doesn’t tell you whether you should accelerate depreciation this year, how to structure your new side hustle to minimize self-employment tax, or which new 2025 credits you qualify for. Those decisions are where the real savings live.

-

Most clients see $5,000–$25,000 in tax savings or avoided penalties in the first year alone, especially once revenue is over $200,000 or they have rental properties, investments, or employees. The ROI is usually 5–10× the fee for anyone with even moderate complexity.

-

It depends on your needs. National firms are great for Fortune 1000 compliance. Local firms usually offer better pricing, faster response times, and deeper knowledge of Colorado-specific rules and auditors. For most businesses under $10 million, local wins.

Read more…