Capital Gains Tax on Business Sales: Calculation, Reduction Strategies, and Impacts

Selling a business is the culmination of years or decades of hard work. For most owners, it’s the single largest payday of their lives. Yet far too many walk away stunned by how much disappears to taxes. A seven-figure sale can easily trigger a six- or even seven-figure tax bill if you aren’t prepared.

The difference between paying 5% and 45% effective tax on your life’s work usually comes down to planning that starts two, three, or even five years before the closing date.

This in-depth guide (updated for 2025) breaks down exactly how capital gains tax works on the sale of a business, the new 2025 rate brackets, the hidden taxes that catch most owners off guard, and, most importantly, the real-world strategies successful founders are using right now to dramatically reduce or eliminate the tax.

How Capital Gains Tax Is Calculated When You Sell a Business

The math is straightforward, but the details trip people up constantly.

Capital Gain = Sale Price − Adjusted Basis

Your adjusted basis is your original purchase price (or the value when you started the company) plus capital improvements minus any depreciation or Section 179 deductions you’ve claimed.

That last part is critical. Every depreciation deduction you took to lower your taxes over the years now increases your taxable gain dollar-for-dollar when you sell. This is called depreciation recapture, and it’s taxed at ordinary income rates (up to 37% in 2025), not the lower capital gains rates.

Assets held longer than one year qualify for long-term capital gains treatment. Almost everything in a mature business, goodwill, customer relationships, equipment, and trademarks, falls into this category.

For a deeper dive with real examples and worksheets, see our complete guide to calculating capital gains tax.

2025 Long-Term Capital Gains Tax Rates and Thresholds

The IRS increased the brackets by roughly 2.8% for inflation in 2025. Here’s what they look like now:

| Filing Status | 0% Bracket | 15% Bracket | 20% Bracket |

|---|---|---|---|

| Single | $0 – $47,025 | $47,026 – $518,900 | $518,901 + |

| Married Filing Jointly | $0 – $94,050 | $94,051 – $583,750 | $583,751 + |

Remember: The gain itself counts toward these income thresholds. A $2 million gain can push a married couple from the 15% bracket all the way into the 20% bracket in the year of sale.

Add in the 3.8% Net Investment Income Tax (kicks in above $250,000 MAGI for married filers) and state taxes, and the effective rate on the top slice of gain often exceeds 30% even before depreciation recapture.

The Two Taxes Most Business Sellers Never See Coming

Depreciation Recapture – Taxed at ordinary rates up to 37% (plus 3.8% NIIT in most cases).

Net Investment Income Tax (NIIT) – An extra 3.8% on virtually every sizable sale.

These two alone can turn what looks like a 20% federal capital gains bill into a 44–48% nightmare on portions of the gain.

The Most Powerful Ways to Reduce (or Eliminate) Capital Gains Tax in 2025

1. Qualified Small Business Stock (QSBS) – Up to 100% Exclusion

This is still the single best tax break available to private business owners. If your company qualifies as QSBS (generally a C-corporation with less than $50 million in assets when the stock was issued), you can exclude the greater of $10 million or 10× your basis from federal tax—100% tax-free.

Yes, LLCs and S-Corps can restructure into C-Corps years ahead of a sale to become eligible. A good tax accountant in Denver or a nationwide specialist can walk you through the process and confirm eligibility long before you ever list the company.

2. Installment Sales – Spread the Pain Over Years

Structure the deal so the buyer pays you over time (usually 3–10 years). You only pay tax as you receive principal payments. This keeps you in lower brackets each year and lets the untaxed money keep working for you.

You must charge adequate interest (the IRS publishes the minimum each month), and there’s default risk, but it remains one of the simplest and most underused tools.

3. Charitable Remainder Trusts (CRTs)

Transfer your shares or ownership interest to a CRT before the sale. The trust sells tax-free, then pays you (and/or your spouse) an income stream for life or a term of years. You get an immediate charitable deduction, avoid all capital gains tax, and convert the sale into tax-efficient lifetime income.

Many founders who want to support causes anyway find this is the closest thing to “having your cake and eating it too.”

4. Opportunity Zones – Defer + Potentially Eliminate Future Tax

Invest your gain into a Qualified Opportunity Fund within 180 days, and you defer tax until December 31, 2026. Hold the new investment for 10 years, and all post-investment appreciation is permanently tax-free.

This strategy exploded after 2017 and continues to be popular for owners who want to stay in real estate or venture-style investments.

5. 1031 Exchanges for the Real Estate Piece

If your business owns valuable real estate, separate it into its own entity well before the sale. You can then 1031 exchange the property portion tax-free while selling the operating business separately.

6. State Tax Planning – Sometimes the Biggest Savings of All

Nine states have no personal income tax. Moving your tax domicile to Florida, Texas, Tennessee, Nevada, etc., even for just the year of sale, can eliminate 5–13+% in state capital gains tax.

Colorado residents, in particular, face a flat 4.4% state tax on the gain. That’s an easy six figures on a multimillion-dollar exit.

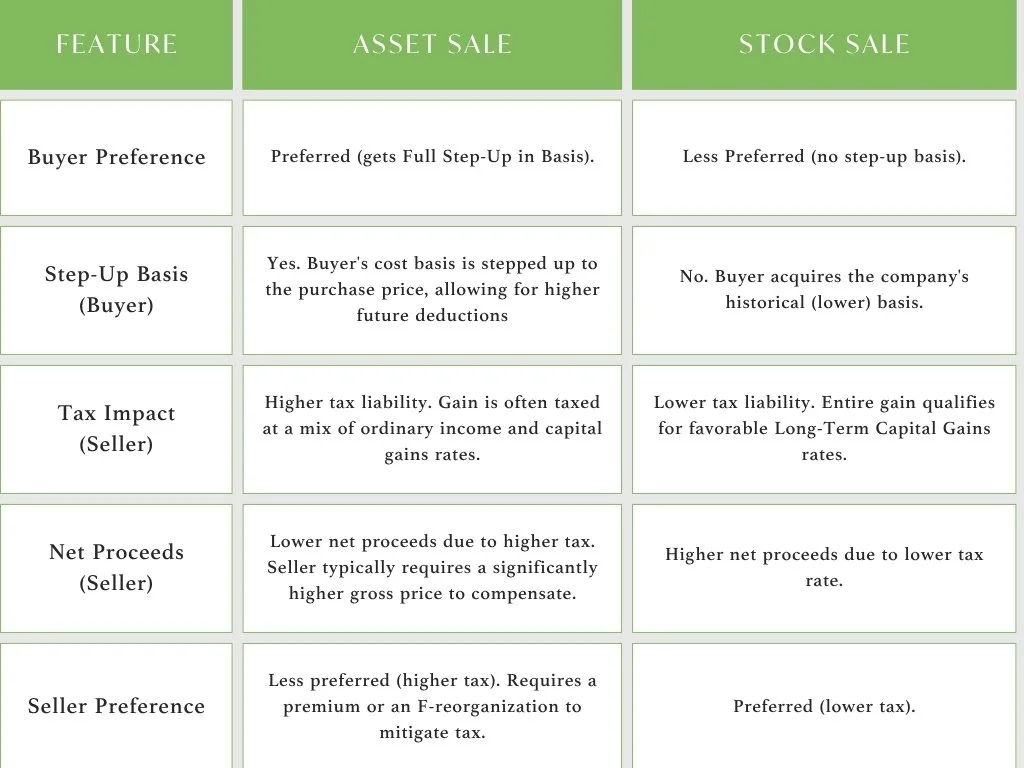

Asset Sale vs. Stock Sale: Why It Matters More Than Ever

Buyers almost always want an asset purchase because they get a full step-up in basis. Sellers almost always want a stock sale because the entire gain qualifies for long-term capital gains rates.

The tax difference is frequently $500,000 to $3 million+. Smart sellers either:

Negotiate a significantly higher price for an asset deal, or

Use an “F-reorganization” to give the buyer the tax benefits of an asset purchase while the seller still receives stock-sale treatment.

Timing Your Exit: 2025 vs. 2026 and Beyond

The current favorable long-term capital gains rates are scheduled to sunset after December 31, 2025. Unless Congress extends them, starting in 2026, the top rate jumps to 39.6% + 3.8% NIIT = 43.4%, and the 15%/20% brackets shrink dramatically.

Many owners who have been “waiting for one more good year” are now accelerating sales into 2025.

Real-Life Example: From $4.1 Million Tax Bill to Under $600k

A Denver-based SaaS company sold for $18 million in early 2025.

Original structure (asset sale, no planning): ≈$4.1 million combined federal + Colorado tax.

After planning: Converted to C-corp six years earlier → $10 million QSBS exclusion. Remaining $8 million structured as a seven-year installment sale + partial CRT.

Final tax: ≈$580,000 total.

Net savings: $3.5 million kept by the founders.

These aren’t hypothetical loopholes these are documented strategies we implement for clients every year through our business tax return service.

Don’t Leave Millions on the Table

The purchase price is only half the story. What you keep after taxes is what actually changes your life.

Too many owners negotiate a great valuation, then hand over 30–45% to the IRS and their state because they never planned. The ones who keep the most simply treat their exit with the same focus they gave to building the company.

Qualified Small Business Stock, installment sales, charitable trusts, Opportunity Zones, state residency planning, these aren’t loopholes. They’re legal, proven strategies used by thousands of founders every year.

Most of them require action months or years before closing.

If you’re even thinking about selling in the next few years, one conversation now can be worth seven figures later. Our firm provides professional accounting services tailored specifically to business owners facing exactly this situation, whether you’re in Colorado or anywhere else in the U.S.

You built something extraordinary. Make sure you get to keep it.

Frequently Asked Questions

-

The Qualified Small Business Stock (QSBS) exclusion under IRC Section 1202 remains the gold standard. If you hold eligible C-corporation stock for at least five years, you can exclude up to $10 million (or 10× basis) of gain 100% from federal tax—and in most states as well.

-

Yes, unless Congress acts. The current 0%/15%/20% structure sunsets after December 31, 2025. Starting in 2026 the top long-term rate reverts to 39.6% + 3.8% NIIT (43.4% total) for high earners, and the lower brackets shrink significantly.

-

Yes, but many PE firms resist seller notes. When they do agree (or when you sell to an individual or strategic buyer), installment treatment is still one of the simplest ways to spread the gain over multiple years and stay in lower tax brackets.

Read more…