Rental Property Taxes: Deductions, Capital Gains, Liens, Deeds, and Landlord Strategies

Being a landlord in 2025 is still one of the best ways to build long-term wealth, but the tax side can feel like a moving target. Between rising property values, new deduction rules, and the ever-present threat of a surprise tax bill, it’s easy to leave money on the table or, worse, get hit with penalties. I’ve worked with hundreds of rental property owners through my practice at Tottax, and the same questions keep coming up: How do I lower my rental property taxes? What happens if I add my kid to the deed? Should I pay a huge property tax bill all at once or look into property tax loans?

Let’s walk through everything you need to know this year, step by step, so you can keep more of what you earn.

1. Rental Income Tax Basics: What’s Taxable and What Isn’t

Every dollar of rent you collect is considered rental income by the IRS and must be reported on Schedule E of your Form 1040. Security deposits are not income if you plan to return them, but if you keep part or all of it because of damage or unpaid rent, that portion becomes taxable in the year you keep it.

The good news? You get to subtract virtually every ordinary and necessary expense before you pay tax on the net number. Common deductions include mortgage interest, property insurance, repairs, utilities you pay, management fees, advertising, and even the mileage you drive to check on the property.

Pro tip for 2025: The bonus depreciation phase-out is now at 20% (down from 40% last year), so if you buy appliances, carpet, or furniture for your rental, you can still write off 20% immediately instead of spreading it over five or seven years. Pair that smartly with cost segregation studies on larger properties, and you can still create massive paper losses even when cash flow is positive.

2. Deducting Rental Property Taxes Like a Pro

Property taxes themselves are fully deductible on Schedule E, no itemized deduction needed. That’s huge because the SALT cap still sits at $10,000 for itemizers, but rental property taxes flow straight through without hitting that limit.

A few lesser-known deductions that save my clients thousands every year:

Homeowners association or condo fees (if you rent the unit)

Legal and professional fees (evictions, lease drafting, accountant fees)

Casualty losses from storms or tenant damage (above the insurance reimbursement)

Travel expenses to real estate conferences or to view new investment properties

If you actively participate in managing the property (making management decisions, approving tenants, etc.), you can still deduct up to $25,000 of rental losses against ordinary income if your modified AGI is under $150,000. That rule didn’t go away in 2025, even though many landlords think it did.

3. Who Actually Pays Council Tax on a Rental Property?

In the U.S. we don’t have “council tax” like the UK, but the equivalent question is who is responsible for property taxes when a home is rented. The legal owner remains liable for the tax bill no matter what. You can write the lease however you want (tenant pays, owner pays, or split), but if the tenant doesn’t pay and you passed the obligation to them, the county will still come after you, not the tenant.

My advice: In single-family rentals, I usually include property taxes in the rent and pay them myself. It keeps the relationship smoother and avoids liens. In multi-family or commercial, reimbursing through triple-net (NNN) leases is standard.

4. Property Tax Loans: A Lifeline or a Trap?

Sometimes life throws a curveball, and the November property tax bill hits harder than expected. That’s where property tax loans come in. A lender pays your delinquent taxes to the county, removes the immediate lien threat, and you repay the lender over 5–10 years at interest rates usually between 9–18%.

The pros:

Stops penalties and interest from the county (which can hit 18–48% per year, depending on the state)

Keeps your credit clean

Gives you breathing room to refinance or sell on your timeline

The cons:

You’re trading a low-interest (or zero if paid on time) county bill for a high-interest private loan

Some lenders sneak in huge origination fees

Only use these as a last resort. If you’re considering one, talk to a personal tax accountant in Denver or wherever you own property first; we can often find better cash-flow solutions through professional tax services.

5. Tax Deed vs Tax Lien: What Investors and Owners Need to Know

Counties use two main methods when owners fall behind on property taxes:

Tax liens: The county sells the lien (the right to collect the back taxes plus interest) to an investor. You still own the property, but if you don’t pay the investor back within the redemption period (1–3 years in most states), the investor can foreclose.

Tax deeds: The county simply auctions the property itself to the highest bidder once the redemption period ends. You lose the house completely.

For accidental landlords who inherited a property or got stuck with a high tax bill, understanding whether your state is a tax lien state or a tax deed state is critical. Florida, Illinois, and New Jersey are big lien states. Texas, Georgia, and much of California lean toward tax deeds.

6. The Hidden Tax Consequences of Adding a Name to the Deed

A lot of parents want to add their adult child to the deed “just in case” or to help them build credit. Stop right there.

When you add someone to the deed without them paying fair-market value, the IRS treats it as a gift. In 2025 the annual gift exclusion is $18,000 per person. Anything above that eats into your lifetime estate/gift tax exemption ($13.99 million this year, but scheduled to drop dramatically in 2026 unless Congress acts).

Even worse: Your child inherits your original cost basis. If you bought the house for $100,000 and it’s worth $800,000 when you die, they get a step-up in basis to $800,000 and pay little or no capital gains tax when they sell. Add them to the deed while you’re alive and they’re stuck with your $100,000 basis. That’s potentially six figures in extra tax.

If your goal is to avoid probate or protect the property long-term, talk to someone who offers tax planning services before you touch the deed. There are far cleaner ways (transfer-on-death deeds, living trusts) that don’t trigger these headaches.

7. Capital Gains Tax on Rental Property: How to Pay Zero (Legally)

Yes, you read that right. There are still several ways to sell a rental property in 2025 and owe zero capital gains tax:

1031 exchange: Roll the proceeds into a bigger or better rental within 180 days. You can do this forever and defer tax until you die (then your heirs get the step-up in basis).

Primary residence exclusion (rare for rentals): If you move into the rental and live there as your main home for at least two of the last five years, up to $250,000 ($500,000 married) of gain is tax-free.

Opportunity Zone investment: Defer tax until 2026 and get a 10% basis step-up if you hold 5+ years, then zero tax on future appreciation if you hold 10 years.

Installment sale: Let the buyer pay you over several years and spread the gain (and tax) out.

Depreciation recapture still applies at 25% on the amount you deducted, but that’s usually far less painful than the full 15–23.8% long-term capital gains rate plus state tax.

8. Rental Income Tax Rate: It’s Not What You Think

There is no special “rental income tax rate.” Your net rental income is added to your other income and taxed at your ordinary marginal bracket (10–37%). Passive activity loss rules still limit losses for high earners, but real estate professionals who spend 750+ hours per year and more than 50% of their working time in real estate activities can deduct unlimited losses against ordinary income. That designation alone saves doctors and tech employees six figures every year.

9. Smart Landlord Tax Strategies

Entity structure matters: Single-member LLCs are still disregarded for tax purposes, but moving rentals into separate LLCs or series LLCs protects you and can help with estate planning.

Short-term rental loophole: If your average stay is 7 days or less (think Airbnb), you may avoid passive loss limitations entirely and deduct losses against W-2 income even if you’re a high earner.

Cost segregation + bonus depreciation: Even with the phase-out, an $800,000 duplex can still generate $100,000–$150,000 in first-year deductions.

Energy credits are back: New efficient HVAC, windows, or solar panels can earn 30% federal credits plus local rebates.

Hire pros early: The best results come when you sit down for personal tax services in January, not April 14.

Final Thoughts

Owning rental property remains one of the most tax-advantaged investments in America, but only if you stay proactive. A single conversation with the right team can save you tens or even hundreds of thousands over the life of your portfolio. Whether you’re just starting out or you already own a dozen doors, Tottax specializes in helping landlords nationwide pay the least amount allowed by law, legally and ethically.

Frequently Asked Questions

-

Yes, but only the net amount you actually pay. If the tenant reimburses you $5,000 in property taxes through additional rent or CAM charges, you report the $5,000 as income and deduct the $5,000 you paid to the county. It washes out.

-

Almost always yes. Most property tax loans have no prepayment penalty and charge 12–18% interest. Paying it off with a HELOC at 7–9% or cash saves a bundle.

-

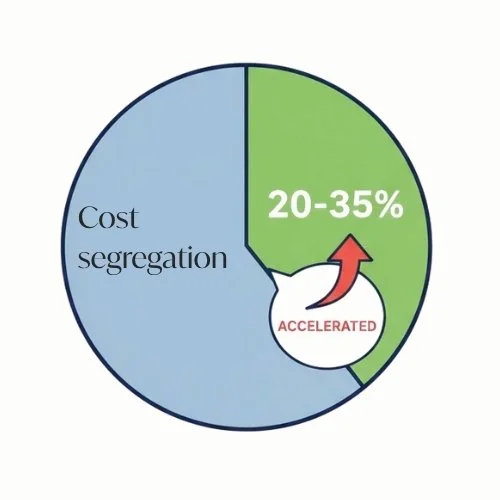

On a typical $500,000 single-family or small multi-family purchase, a good study moves 20–35% of the building cost into 5-year or 15-year property, letting you accelerate depreciation and save $20,000–$60,000 in tax in the first few years (depending on your bracket).

Read more…