Specialized Taxes: Colorado Rules, Inheritance, Child Credits, Deceased Estates, and More

Tax season in Colorado always feels a little different from the rest of the country. Between the TABOR refunds that show up like an unexpected bonus, the complete absence of a state-level inheritance or estate tax, and a generous new child tax credit that rolled out for 2025, there is a lot to unpack this year. Whether you are planning your own return, helping a family member, or stepping in as an executor for an estate, the rules can get complicated fast.

Let us walk through the biggest moving parts so you know exactly where you stand in 2025.

The Colorado TABOR Refund: Your Annual “Tax Surplus” Check

Every few years Colorado voters get a nice surprise in the mail because of the Taxpayer’s Bill of Rights (TABOR). When state revenue exceeds the constitutional cap, the excess has to be returned to taxpayers. In 2025 the mechanism is still the same six-tier system based on your adjusted gross income, but the amounts are larger than most people expected because of strong economic growth in recent years.

Single filers with AGI under $46,000 can see refunds above $800, while married couples filing jointly under $92,000 often get north of $1,600. The refund shows up automatically on your state return as a sales-tax refund mechanism if you file electronically, or you receive a paper check later in the summer. The beauty of the TABOR refund in Colorado is that you do not have to itemize or jump through hoops; just file your return on time and the Department of Revenue does the rest.

If you moved into Colorado recently, make sure you file a full-year resident return even if you only lived here part of the year. Part-year residents still qualify for a prorated amount. For the latest numbers and exact income tiers, the Colorado Department of Revenue updates the table every January.

Colorado Inheritance Tax and Estate Tax: The Non-Event That Still Surprises People

Here is the headline most out-of-state heirs love to hear: Colorado has no state inheritance tax and no state estate tax in 2025. Zero. Nada. That means if you inherit money, property, or investments from a Colorado resident, the only estate tax you might owe is the federal one, and that only kicks in above the 2025 federal exemption of $13.61 million per person (or $27.22 million for a married couple with proper portability).

People moving from states like Pennsylvania, New Jersey, or Maryland are usually stunned. They are used to seeing 4-16% sliced off inheritances for the state. Not here. The absence of an inheritance tax in Colorado is one of the quiet financial advantages of living (or dying) in the Centennial State.

That said, executors still have plenty of federal paperwork if the estate is large, and you will want a Colorado tax accountant who understands both state and federal rules to avoid surprises. Even though Colorado itself does not take a cut, the IRS still wants its final 1041 return and possibly a federal estate tax return (Form 706).

Child Tax Credit and Family Affordability Credit: Colorado Steps Up in 2025

While the federal Child Tax Credit is still partially refundable at $2,000 per child, Colorado decided to go bigger starting with the 2024 tax year (filed in 2025). The new Colorado child tax credit 2025 can reach $3,200 per child under age 6 for lower-income families, and it is fully refundable. That means even if you owe zero state tax, you still get the full amount as a check.

The income phase-out is generous compared to many states:

Single filers: full credit up to $75,000 AGI, partial up to $85,000

Married filing jointly: full credit up to $115,000 AGI, partial up to $125,000

On top of that, Colorado kept the Family Affordability Tax Credit that launched a couple of years ago. It can add another few hundred dollars for families who qualify for the state Earned Income Tax Credit. When you stack the state credit on top of the federal one, a family with two young children earning $60,000 can easily cut their tax bill by $5,000 or more, sometimes turning a balance due into a nice refund.

If you run a small business and pay yourself through an S-Corp or Schedule C, talk to someone about tax planning services early. The child care contribution credit and the new paid family leave deductions can layer even more savings on top.

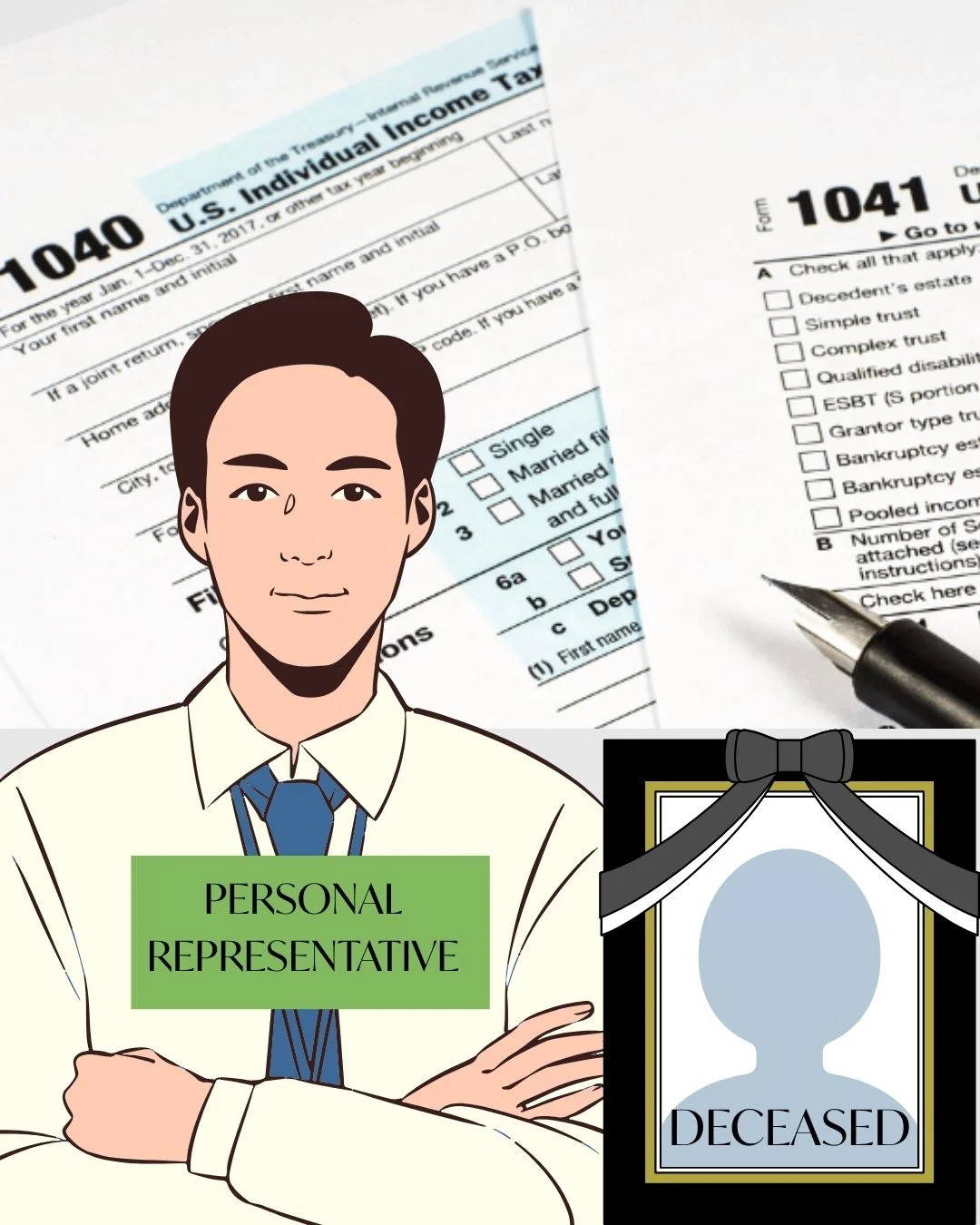

Who Is Responsible for Paying Taxes for a Deceased Person?

When someone passes away, the tax responsibilities do not disappear. The executor or personal representative is legally on the hook for filing the deceased’s final 1040 (and Colorado 104 if they were a resident) for the year of death. That return covers January 1 through the date of death and reports all income earned up to that point: wages, interest, dividends, retirement distributions, even capital gains from sales that closed before death.

If the decedent was married, the surviving spouse can usually file a joint return for that final year, which often saves money because of the wider brackets and double standard deduction.

After the final personal return, the estate itself becomes its own taxpayer. Any income earned after death (interest on bank accounts, rent from properties, dividends) gets reported on Form 1041 (and Colorado DR 0104 if the estate is large enough). The executor signs these returns and can be personally liable if they distribute assets before paying taxes owed.

That is why the importance of accounting for executors cannot be overstated. Sloppy records can lead to penalties, delayed distributions, and family fights. Many executors quickly realize they need professional accounting services to keep everything straight and avoid costly mistakes.

Personal Loans and Taxes: What Most People Get Wrong

One question we hear every year: “Can I deduct the interest on my personal loan?” The short answer is almost never. Unlike mortgage interest or student loan interest, interest on a plain personal loan (signature loan, debt consolidation loan, etc.) is not deductible on Schedule A.

There are two big exceptions:

If you use the loan strictly for business purposes or investment purposes, the interest can become deductible on Schedule C or Schedule E.

If you borrow against a life insurance policy with cash value, that interest can sometimes be deducted if you meet strict IRS rules.

Otherwise, treat it as personal interest: nondeductible. The confusion usually comes from credit-card debt or “buy now, pay later” plans that feel like loans but are treated the same way for tax purposes.

Staying Sharp: Accounting and Tax Conferences Worth Attending

Even though most 2024 conferences have wrapped up, the knowledge from this year’s events is still fresh and directly applies to 2025 filings. The big themes we saw at the AICPA Engage, Scaling New Heights, and the Colorado Society of CPAs Tax Conference were automation, real-time payroll for remote workers, and the explosion of state-specific credits like the ones we just covered.

If you are a business owner or independent contractor, mark your calendar for the 2025 versions. The networking alone can save you thousands when you find a new deduction or credit you did not know existed.

Putting It All Together for 2025

Colorado remains one of the more taxpayer-friendly states when you look at the big picture: no inheritance or estate tax, healthy TABOR refunds, and aggressive family credits. But the rules are rarely simple. A qualified personal tax advisor who actually practices in Colorado can spot opportunities (and traps) that generic online software will miss.

Whether you are expecting a TABOR check, inheriting assets, claiming the expanded child tax credit, settling an estate, or just trying to figure out if any of your personal loans create a deduction, the devil is always in the details.

If any of this feels overwhelming, you are not alone. Reach out to a local Colorado tax accountant or explore professional accounting services before the April deadline sneaks up. A little planning now usually means a lot more money back in your pocket later.

Frequently Asked Questions

-

No. Colorado has no state-level inheritance tax and no state estate tax. Only the federal estate tax applies, and only for estates larger than $13.61 million per person in 2025.

-

Low to moderate-income families can receive up to $3,200 per child under age 6. The credit is fully refundable and phases out starting around $75,000 AGI for singles or $115,000 for married couples.

-

The executor or personal representative files the deceased’s final individual income tax return (federal 1040 and Colorado DR 104) for the year of death. The estate may also need its own returns (Form 1041) if it earns income after death.

Read more…